Guest post: Hundreds of planned coal mines ‘incompatible with 1.5C target’

Those are the key findings of Global Energy Monitors initially detailed study of global coal mine propositions, based upon data from our brand-new Global Coal Mine Tracker.

Plans to massively boost coal production are, for that reason, incompatible with the 1.5 C limit. If worldwide environment objectives are to be met, the approximated $91bn of financial investment in the proposed mines might be left stranded.

We discovered more than 400 new mine propositions that might produce 2,277 m tonnes per year (Mtpa), of which 614Mtpa are already being established. The strategies are greatly concentrated in a few coal-rich regions throughout China, Australia, India and Russia.

Yet last month, the International Energy Agency said no brand-new coal mines– nor extensions of existing mines — were “needed” in its pathway to 1.5 C. A UNEP report in 2015 said coal output should fall 11% each year to 2030, under the same target.

Propositions to develop numerous new coal mines might raise international output of the nonrenewable fuel source by 30%, putting the worlds climate goals or up to $91bn of financial investment at danger.

If they all went on, the brand-new mines might provide as much as 30% of existing international coal production — or the combined output of India, Australia, Indonesia and the US.

Tracking the worlds coal mines

We set a capacity limit of 1Mtpa or higher for proposals in the GCMT. This screened out smaller sized jobs and life extensions that would lengthen a mines operation, but not increase its output.

This consisted of a systematic evaluation of federal government ministry information, public allowing applications, corporate annual reports, news statements and press releases.

The new Global Energy Monitor Global Coal Mine Tracker (GCMT), released in June 2021, is a comprehensive database of the worlds proposed and active coal mines.

The tracker lists mines by nation, region, greenhouse gas emissions and ownership. It likewise covers all proposals of a minimum of 1Mtpa, totaling up to 432 developments throughout 413 sites.

We judged active progress on a case-by-case basis: was a task conference permitting due dates? Were companies still reporting activity on the task? Were they still noting it in their annual reports? Did neighborhoods on the ground report activity at the mine site?

To track brand-new proposals, our scientists sourced an initial project list of every revealed, checked out, permitted and under building and construction coal mine worldwide.

Our last list tallied 432 active coal mine propositions and mine growth tasks around the world, totalling 2,277 Mtpa of new capability.

The GCMT includes all running mines that produce more than 5Mtpa — some 433 mines in overall, accounting for around 60% of overall international output. By 2022, it will also cover existing mines of a minimum of 1Mtpa, expanding protection to 1,800 mines and over 90% of output.

We considered a task shelved and removed it from the list if it went dark after 2 years– for example, if it had been scrubbed from a company site, lapsed in permitting, or was failing and struggling to get financing.

This is comparable to 30% of existing output, which is expected to reach 7,575 Mtpa in 2021.

We then examined each proposition, extracting older and shelved jobs from those that have signified continuous progress or motion in the previous two years.

The capability threshold likewise omitted one of the most pie-in-the-sky statements that lacked even the basics of a mine strategy– a necessary precondition to estimate recoverable reserves, operating expenses and to satisfy potential financiers..

Where are the new mines?

These plans have yet to undergo the build-out of mine infrastructure, making them especially vulnerable to cancellation.

On the other hand, the bulk of Indias propositions are sited in simply 3 states: Jharkhand (161Mtpa), Odisha (112Mtpa) and Chhattisgarh (40Mtpa), which together comprise 77% of all the coal development in South Asia.

Unlike China, where 74% of organized jobs are already under building and construction, the large bulk of proposed mining capability in Australia (94%), India (96%) and Russia (80%) remains in the earlier pre-construction stages of advancement.

The concentration of coal mine propositions perpetuates the broader trends in coal production over the previous five years. with production in China, India, Australia and Russia steady or rising, even as it decreases in many historic coal manufacturers, such as the United States, UK and EU..

The 10 subnational states and provinces with the biggest pipeline of coal mine proposals, Mtpa. Source: Global Coal Mine Tracker, Global Energy Monitor, January 2021. Chart by Carbon Brief utilizing Highcharts.

The hectic construct out in China, which leads the world in new mine developments, is driven by just four provinces: Inner Mongolia, Xinjiang, Shanxi and Shaanxi. These provinces alone represent 89% (544Mtpa) of all the proposed capability in China.

Likewise, the coal-rich Kuznetsk Basin (Kuzbass) in Kemerovo Oblast, makes up over one-third (105Mtpa) of all new mine propositions in Russia.

The nationwide view masks the origins and density of these mine tasks.

Queensland, Australia has more coal under advancement than any subnational state or province on the planet (357Mtpa), boosted by a selection of jobs in the Bowen and Galilee Basins.

The same is true for new mine developments in Australia, India and Russia, where mining activity is greatly clustered in conventional coal-mining areas, displayed in the chart below.

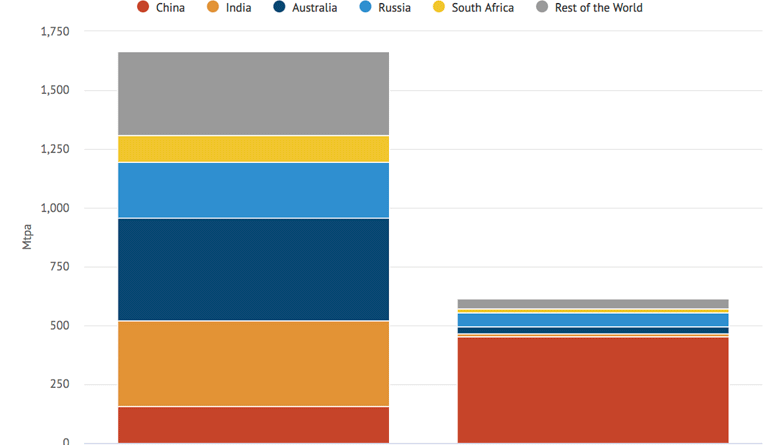

International coal mining capability, Mtpa, in the early stages of advancement (left column) and already under construction (right), broken down by nation. Source: Global Coal Mine Tracker, Global Energy Monitor, January 2021. Chart by Carbon Brief utilizing Highcharts.

This is displayed in the chart below, which likewise highlights the reality that almost three-quarters of capability already under building and construction is situated in China.

More than three-quarters of proposed new capacity is clustered in just 4 nations: China (609Mtpa); Australia (466Mtpa); India (376Mtpa); and Russia (299Mtpa).

The 432 mine proposals, representing 2,277 Mtpa of potential brand-new capability, are highly focused in simply a handful of coal-producing nations and areas.

Who is planning new coal mines?

The pattern appears worldwide: among the biggest manufacturers, just Russia has more expansions on the books than greenfield tasks.

The Production Gap Report estimated that coal production would need to decline 7% every year under a “well listed below” 2C path and by 11% for 1.5 C..

Sharelines from this story.

CompanyProposed Mine Capacity (Mtpa).

Our Global Coal Mine Tracker extends this analysis by providing asset-level coal mine information to compare against Paris-compliant pathways.

At this size, they are less vulnerable to the intense public scrutiny generally connected with coal megaprojects, while also being protected from near-term combination and closure plans, particularly in China and India, where national governments have signalled plans to decrease the number of small mines in their portfolios.

Especially, the overall of brand-new coal-mining capability that we determined, at some 2,277 Mtpa, is close to the 2030 limit in UNEPs 1.5 C path, recommending almost all existing mines would need to close this decade if the proposed tasks are completely developed.

Even if only the mines presently being constructed are developed, coal output in 2030 would stay three times above the level in UNEPs 1.5 C path.

NLC India (India) 34.

In part, the size of these jobs seems to have produced a “Goldilocks” result: a lot of are in the mid-range, neither extremely small nor extremely large, with a median capacity of 3.5 Mtpa.

SibAnthracite Group (Russia) 31.

The pursuit of the new coal-mining projects we identified could squander billions of dollars in capital investment or make global climate goals unattainable.

Despite political, financial and social pressures on the coal market, existing production levels and the variety of brand-new mine proposals recommend the world is not on course to phase out coal fast enough to avoid the worst effects of international climate modification.

While there are prominent cases of resistance to new greenfield mines — such as the Adani Carmichael mine in Australia — numerous in our dataset have flown under the radar.

This is displayed in the chart below, where historic coal output (black) is predicted forward presuming all coal mine proposals are developed by 2030 or only those already under construction are constructed (shades of red) or in pathways for 1.5 C or 2C (blue).

Taking a look at the 2,277 Mtpa of proposed new coal mining capability in regards to ownership, some 388 personal business and state-owned enterprises are involved.

Our asset-level forecasts are similar to those in UNEPs international forecast, along with the “middle of the roadway” coal production situation utilized in IPCC design paths.

The sponsors of these brand-new coal mines face substantial stranded asset risk. If planned coal mines open as planned, but are required to lower production levels or closed down early, we estimate they represent approximately $91bn in stranded possessions, based upon the typical capital expenses to open a coal mine.

( In North America, the numbers are reversed, with metallurgical coal for steelmaking accounting for 70% of proposed capacity.).

China Coal (China) 32.

The top 10 designers of proposed brand-new coal mine capability, Mtpa. Source: Global Coal Mine Tracker, Global Energy Monitor, January 2021.

China Datang (China) 50.

This is not to say the largest producers have actually chosen out, with major companies still bought brand-new developments worldwide. But it is noteworthy that several small and medium firms — especially in Australia — have actually elbowed their way into a list of the top 10 developers, revealed below..

If all 2,277 Mtpa of proposed coal-mining capability were to open, then output in 2030 would be three times the level in UNEPs 2C pathway and four times as high when it comes to 1.5 C.

VostokCoal (Russia) 35.

Mineralogy (Australia) 106.

Yet even private coal companies remain committed to new tasks, regardless of market headwinds. Our data reveals that among private developers, independent and small firms are revealing a greater cravings for new mine jobs than multinationals.

Coal India (India) 243.

Around two-thirds of the suggested jobs, some 298 mines, would be “greenfield” developments at brand-new areas, as opposed to growths of existing sites.

Incompatible with 1.5 C.

Where coal type is understood, thermal coal represent 71% of the prepared capability we recognized, while metallurgical coal for steelmaking accounts for 20% and mixed for 9%.

Adani Group (India) 67.

The metric of a “production gap”, very first developed by the UN Environment Program (UNEP) and numerous partners in 2019, clarified the disparity between organized fossil fuel production and the decreases required to satisfy the Paris environment contract.

Glencore (Switzerland) 45.

In China and India, most of the worlds proposed coal mines are sponsored by state-owned business, entirely or partially owned by the federal government, meaning taxpayer money continues to subsidise mine projects to fuel provincial and state economies..

Source: Global Coal Mine Tracker, Global Energy Monitor, January 2021. The 10 subnational states and provinces with the largest pipeline of coal mine proposals, Mtpa. Source: Global Coal Mine Tracker, Global Energy Monitor, January 2021. The projections account for 306Mtpa of capacity from mines anticipated to close or tire their reserves prior to 2030. Sources: Historic information from BGR Energy Study 2019, planned and building and construction from the Global Coal Mine Tracker and paths for 1.5 C or 2C from UNEPs 2020 Production Gap report.

Valiant Resources (Australia) 48.

If all proposed capacity in our tracker is realised, coal production might reach 10,100 Mtpa by 2030 — more than four times the 2,400 Mtpa in UNEPs 1.5 C pathway and around 3 times the 3,600 Mtpa in its “well-below” 2C circumstance.

Much more striking is that new thermal coal mines control advancement strategies, in spite of coal-fired power generation having remained in decline considering that 2018.

Historical worldwide coal output, Mtpa (black) and forecasts assuming all organized tasks proceed or just those currently being built (red, pink) relative to pathways for 1.5 C or 2C (blue). The projections represent 306Mtpa of capacity from mines expected to close or tire their reserves before 2030. They assume proposed capacity opens evenly throughout the years to 2030. Sources: Historic information from BGR Energy Study 2019, prepared and building from the Global Coal Mine Tracker and paths for 1.5 C or 2C from UNEPs 2020 Production Gap report. Chart by Carbon Brief using Highcharts.