Analysis: China’s carbon emissions grow at fastest rate for more than a decade

The steel industrys proposed targets have significant significance for Chinas emissions trajectory.

Steel industry emissions targets.

CO2 emissions estimates are based on National Bureau of Statistics default calorific worths of fuels and IPCC default emissions elements. Cement CO2 emissions element is based upon 2018 information.

The targets leave space for emissions to increase by around 5– 10% from 2020 to 2025, depending upon the GDP growth rate. Additionally, the five-year period is viewed as an essential time window to lead the way for emissions to peak and begin decreasing rapidly in the 2nd half of the years.

Steel production in 2020 was 40% higher than forecasted in the previous five-year strategy in 2016, for example. Steel production broadened by 31% over the duration, while the GDP broadened 32%.

In the very first quarter of 2021, Chinas CO2 emissions from nonrenewable fuel sources and cement production grew by 14.5%, relative to the exact same period a year earlier.

Fastest development.

The CO2 surge reflects a rebound from coronavirus lockdowns in early 2020, however also a post-Covid economic recovery that has up until now been dominated by development in steel, building and construction and cement.

If emissions in 2021 as an entire match the growth seen over the past 12 months, there would be little room for more boosts to 2025, under the targets of Chinas 14th five-year strategy (14FYP).

Annualised Chinese CO2 emissions from fossil fuels and cement, by source, given that 2010, millions of tonnes per year. Emissions are estimated from National Bureau of Statistics information on production of different fuels and cement, China Customs data on exports and imports and WIND Information information on modifications in stocks, applying IPCC default emissions aspects and annual emissions elements per tonne of cement production till 2018.

The numbers mentioned in conjunction with the emissions target suggest that only direct emissions from iron and steel production are included, not electricity usage for manufacturing of steel items or electrical steelmaking from scrap. Yet, the target still has ramifications that likewise go beyond steel.

If CO2 kept going up at the current rate up until the end of 2021– a roughly 9% annual boost from 2019 — then there would be practically no area for more emissions growth throughout 2022-2025, meaning emissions would need to remain flat or be up to meet the 2025 targets.

Main figures reveal the location of floor area under building increased by 13% in the first four months of 2021, compared with 2019.

One sign that this might be possible originates from the steel sector propositions themselves.

The primary chauffeur of steel and other commercial expansion is real-estate building and construction.

The most recent increase helped push Chinas emissions to a new record high of nearly 12GtCO2 in the 12 months to March 2021, as shown in the chart below. This is nearly 600MtCO2 (5%) higher than the total in 2019, which was unaffected by the coronavirus pandemic.

The emissions-intensive healing to date is due to a financial policy response and deeply ingrained financial structures that benefit construction and commercial sectors in a slump.

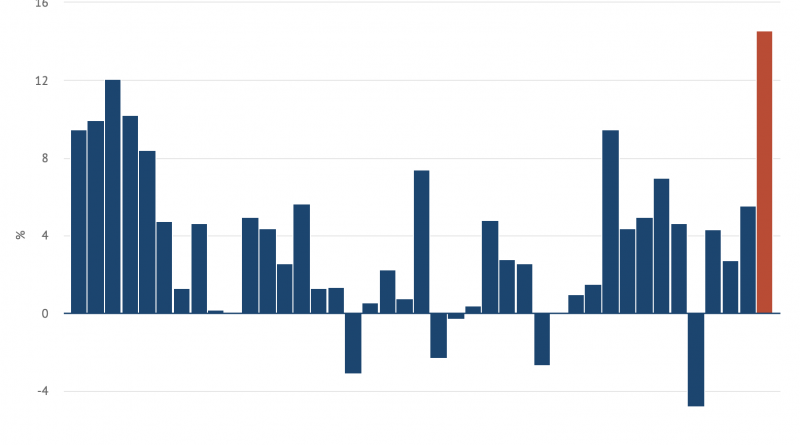

Emissions in the year to March 2021 grew by nearly 7% year-on-year and by 10% relative to the year to March 2019– respectively, the fastest rates since 2012 and 2013.

Sharelines from this story.

These figures are based upon information on evident coal and gas need, and oil production and imports from the National Energy Administration and WIND Information.

Consumer-facing downstream industries are apparently struggling in the middle of weak need and high commodity prices.

Charting the sources of emissions growth.

Many Chinese analysts have noted the divergence between recent growth in genuine estate, significant industries and exports on one hand and consumption on the other.

If steel output volumes level off and the supply of scrap is fully used for steel production, this alone would be enough to deliver a nearly 30% reduction in emissions from the sector– as 30% of main steelmaking and direct emissions would be replaced with electric arc production..

This follows the practice of the majority of existing main statistical reporting and analysis in China.

Power need was driven by industry, where need grew 18%, representing 80% of growth and increasing its share, as reported by China Electricity Council.

These aspects could allow a clampdown on “low-quality growth”, directing financial investments and costs towards services and modern sectors, and reducing the energy intensity of development.

The existing steel industry emission reduction plan, for that reason, rests on China understanding its aspiration for “premium” growth and economic change that is less dependent on building, after the economic policy reaction to Covid-19 caused an obstacle to this effort.

Data sources.

This is shown by the red column in the chart, below. Modifications for previous quarters are in blue, highlighting the impact of coronavirus lockdowns in the first quarter of 2020.

The market can play a role in minimizing or stabilising steel need, because higher quality steel minimizes the amount required in construction.

The strategy to cut steel emissions is primarily predicated on a significant increase in electric steelmaking from scrap metal, potentially reaching nearly 40% of steel output by 2030.

The largest increase in fixed property investment in January-April took location in smelting and pushing of iron and steel metals, based on National Bureau of Statistics information accessed through WIND Information, increasing more than 60% from two years ago and even exceeding investment in medicine production.

The proposals highlight the fact that the overall amount of steel embedded in Chinas capital stock is close to the level where demand is filled in the majority of developed countries.

Nevertheless, the current increase in steel need is already driving investment in brand-new production capacity.

While emissions from Chinas steel sector have been increasing quickly recently, enthusiastic emissions decrease targets are being put in location for the industry.

When information was readily available from multiple sources, different sources were cross-referenced and official sources used when possible, changing data from Wind Information to match.

The analysis is based on main figures for the domestic production, import and export of fossil fuels and cement, in addition to commercial data on modifications in stocks of kept fuel..

The growth of thermal power delivered 73% of the growth in generation total, meaning tidy energy would have required to grow practically 4 times as fast to cover the increase in need.

As an outcome, continued development in steel demand at comparable rates to GDP would lead to increases in coal-based steel supply and emissions, in spite of the sectors proposed targets.

If the need for steel continues to grow as quick as Chinas GDP, then overall need might increase quicker than the level able to be provided by increasing output from scrap. It would also be too large to be fulfilled by strategies to pilot hydrogen and other non-coal-based steelmaking.

This price quote of quarterly emissions growth is consistent with, but rather lower than figures published just recently by the independent Carbon Monitor scholastic research group, which supplies price quotes of “real-time” emissions information.

Even versus the pre-pandemic very first quarter of 2019, January-March 2021 posted development of 9%, revealing that the boost this year is not only a rebound from the effect of lockdowns in 2020.

These targets would involve the sectors CO2 emissions peaking before 2025 and falling 30% from the peak by 2030.

When official releases did not offer modifications from 2019 to 2021, these are determined from the connected release and previous iterations of the same regular release, although just the most recent one is connected to.

Year-on-year modification in Chinas quarterly CO2 emissions from fossil fuels and cement, %. Emissions are estimated from National Bureau of Statistics information on production of various fuels and cement, China Customs data on imports and exports and WIND Information data on modifications in inventories, using IPCC default emissions elements and annual emissions aspects per tonne of cement production until 2018.

The share of non-fossil sources fell because hydropower output decreased 8%, due to variations in rainfall. As an outcome, thermal power generation, dominated by coal, expanded 12%.

Five-year plan challenge.

On this basis, around 70% of the increase in emissions in the very first quarter of 2021 was because of increased usage of coal, with growth in oil demand contributing 20% and fossil gas need 10%.

Based on coal and power usage data cited above, the steel sector is accountable for more than 30% of total coal use in China and has actually been the primary source of development in need.

A device creating steel poles, Laiwu, Shandong, China. Credit: TAO Images Limited/ Alamy Stock Photo.

The International Energy Agency (IEA) forecasted a 6% boost from 2019 to 2021, which would also suggest a downturn to less than 1% annually emissions growth from 2022 onwards.

This compares to the present share of electric steelmaking of just 10%.

Information for the analysis was compiled from the National Bureau of Statistics, National Energy Administration, China Electricity Council and China Customs official data releases, and from WIND Information, an industry information company.

However the emissions decrease plan can only work if the existing expansion of steel need for building slows down. This goes to the heart of Chinas macroeconomic policy.

Year-on-year change in Chinas quarterly CO2 emissions from fossil fuels and cement, %. Emissions are estimated from National Bureau of Statistics information on production of various fuels and cement, China Customs information on exports and imports and WIND Information information on modifications in stocks, applying IPCC default emissions aspects and yearly emissions elements per tonne of cement production until 2018. Monthly values are scaled to annual information on fuel intake in annual Statistical Communiques and to National Energy Administration information on coal and fossil gas intake in the first quarter of 2021. Annualised Chinese CO2 emissions from fossil fuels and cement, by source, since 2010, millions of tonnes per year. Emissions are approximated from National Bureau of Statistics data on production of various fuels and cement, China Customs information on exports and imports and WIND Information data on modifications in inventories, applying IPCC default emissions aspects and yearly emissions elements per tonne of cement production up until 2018.

The pandemic action in the rest of the world has exacerbated the domestic circumstance by increasing Chinese market through need for exports.

Power need in services grew at the same rate as in industry, and cargo and property were among the fastest-growing sectors, acquiring on the back of expansion in construction and industry.

During the past five years, steel demand development considerably exceeded government targets and projections: GDP development was in line with targets, but was much more steel-intensive than anticipated.

The government has actually produced space for structural reforms by setting a GDP target for this year that is well below agreement projections and by not setting a target at all for the coming five years.

A proxy of building and construction activity, the production of lifts, elevators and escalators increased by 85%, based upon information from the National Bureau of Statistics as reported by WIND Information.

For oil usage, just data on oil products intake was readily available so petroleum usage is approximated from production and imports.

Attaining such a slowdown would need rebalancing the pattern of financial recovery.

Furthermore, as noted in the expert reports linked above, the retail and service sectors are beginning to recover, decreasing the requirement for construction costs to keep GDP development, while the credit-fuelled development of the past year has actually resulted in restored issues about debt levels.

Some 60% of the increase in coal usage originated from the power sector, with the metals market (15%) and the building materials sector (10 %, glass and cement) the next largest factors.

The factors for such quick emissions growth in China connect to the method the country has actually come out of the coronavirus pandemic on a wave of stimulus spending.

The goals are the steel industrys suggested reaction to the central federal governments require emissions from major energy-consuming industries to peak by 2025, attain “constant” reductions by 2030 and “considerable” decreases by 2035.

The acceleration in emissions growth presents a possible challenge for conference Chinas 2025 targets for energy strength and non-fossil energy, embeded in the 14th five-year strategy published in March.

In the power sector, total electrical power generation in January-April 2021 increased by 11%, wind by 34%, nuclear 19% and solar 18%, based on National Bureau of Statistics data.

As Covid-19 lockdowns skew the baseline for year-on-year comparisons, nevertheless, this section will be comparing 2021 data to the corresponding periods in 2019.

In 2007, significant steel market groups announced they were going to provide a 100MtCO2 emission reduction through steel recycling and other procedures. What really happened is that steel output and CO2 emissions grew three-fold in the following decade, due to post-financial crisis stimulus.

It should mean a tightening up of building and construction and genuine estate costs that would flex Chinas emissions trajectory downwards if the federal government follows this technique.

Chinas co2 (CO2) emissions have grown at their fastest speed in more than a decade, increasing by 15% year-on-year in the first quarter of 2021, brand-new analysis for Carbon Brief programs.

Unless this investment is directed into electric steelmaking rather than more blast furnaces for coal-based steel, it might be tough to fulfill the sectors proposed emissions targets.

The post-pandemic rise means Chinas emissions reached a new record high of almost 12bn tonnes (GtCO2) in the year ending March 2021. This is some 600m tonnes (5%) above the overall for 2019.